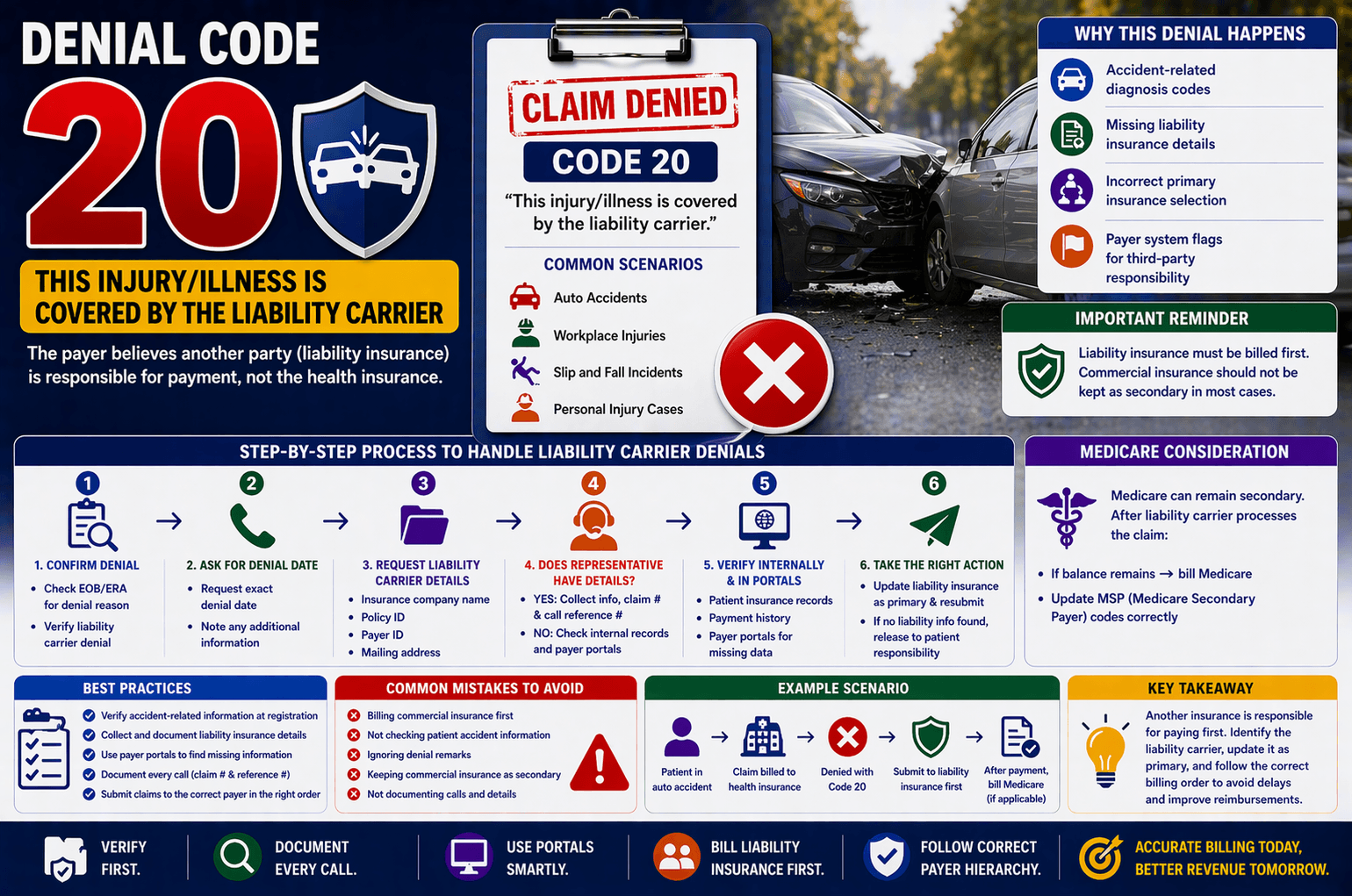

In medical billing, claim denials are common—but each denial comes with a reason that needs careful handling. One such denial is: “This injury/illness is covered by the liability carrier.”

If you’re new to healthcare revenue cycle management (RCM), this message might seem confusing. However, it simply means that another party—usually an insurance linked to an accident or injury—is responsible for paying the claim, not the standard health insurance.

This guide breaks down everything you need to know about liability carrier denials, how to handle them step-by-step, and how to prevent revenue delays.

What Does “Covered by Liability Carrier” Mean?

A liability carrier is an insurance provider responsible for covering medical expenses resulting from accidents or third-party injuries.

Common scenarios include:

Auto accidents

Workplace injuries

Slip and fall incidents

Personal injury cases

When a claim is denied for this reason, it means:

The payer believes another insurance (liability insurance) should be billed first.

Why Do These Denials Occur?

Understanding the root cause helps resolve the issue faster.

Key reasons:

Accident-related diagnosis codes on the claim

Missing liability insurance details

Incorrect primary insurance selection

Payer system flags indicating third-party responsibility

Example:

If a patient visits the hospital after a car accident, their auto insurance (liability carrier) should be billed before their regular health insurance.

Step-by-Step Process to Handle Liability Carrier Denials

Handling these denials requires a structured approach. Here’s how experienced billing professionals resolve them.

- Confirm the Denial

Start by verifying the denial reason:

Check the Explanation of Benefits (EOB) or Electronic Remittance Advice (ERA)

Look for statements indicating liability involvement - Ask for the Denial Date

Contact the payer and request:

Exact denial date

Any additional notes related to the denial

This helps maintain proper documentation and follow-up timelines. - Request Liability Carrier Details

You need complete information about the responsible insurance.

Ask for:

Insurance company name

Policy ID

Payer ID

Mailing address

Without these, you cannot proceed with resubmission. - Check if the Representative Has the Details

At this stage, there are two possible scenarios:

✔ If the Representative HAS Details:

Collect all liability insurance information

Ask for:

Claim number

Call reference number (for documentation)

❌ If the Representative DOES NOT Have Details:

Take the following actions:

Check your internal system:

Patient insurance records

Payment history

Look for:

Any liability insurance listed as primary

Use payer portals (if accessible) to find missing data

What to Do After Gathering Information

Once you have clarity, the next step depends on whether liability details are available.

Scenario 1: Liability Insurance Found

Update the liability carrier as primary insurance

Resubmit the claim to the liability payer

Ensure:

Commercial insurance is not kept as secondary

Keep proper documentation of submission

Scenario 2: No Liability Information Available

If all efforts fail:

Release the claim to the patient responsibility

Inform the patient (if required)

Document attempts made to retrieve liability details

Special Case: Medicare as Secondary Insurance

Medicare follows specific coordination of benefits rules.

Important guidelines:

Medicare can remain secondary

After billing the liability carrier:

If balance remains → bill Medicare

Update:

MSP (Medicare Secondary Payer) codes correctly

Key Tips to Handle Liability Denials Efficiently

To streamline your workflow and reduce errors, follow these best practices:

Always verify accident-related information

Check patient intake forms carefully

Document every call

Record claim number and reference ID

Use payer portals effectively

They often provide missing insurance details

Never assume primary insurance

Confirm before resubmission

Avoid keeping commercial insurance as secondary

This is a common mistake that leads to repeated denials

Practical Example

Let’s simplify with a real-world scenario:

Situation:

A patient visits after a workplace injury.

What happens:

Claim submitted to commercial insurance → Denied

Reason: Covered by liability carrier (Workers’ Compensation)

Resolution:

Contact payer → Confirm denial

Get Workers’ Compensation details

Update insurance as primary

Resubmit claim

Frequently Asked Questions (FAQs)

- What is a liability carrier in medical billing?

A liability carrier is an insurance company responsible for paying medical expenses related to accidents or injuries caused by a third party. - Can I bill secondary insurance without billing the liability carrier?

No. The liability carrier must always be billed first before any secondary insurance. - What if no liability insurance information is available?

If all efforts fail to locate it, the claim can be transferred to patient responsibility. - Why shouldn’t commercial insurance be kept as secondary?

Because liability insurance takes priority. Keeping commercial insurance as secondary can lead to repeated denials. - When should Medicare be billed?

After the liability carrier processes the claim and leaves a balance, Medicare can be billed as secondary—provided MSP codes are updated correctly.

Conclusion:

Liability carrier denials may seem complicated at first, but with a structured approach, they are manageable. The key is understanding that another insurance is responsible and taking the right steps to identify and bill that payer.

By:

Verifying denial details

Gathering complete liability information

Updating insurance correctly

Following proper resubmission protocols

—you can reduce claim delays and improve reimbursement efficiency.

Mastering this process is essential for anyone working in medical billing, as it directly impacts revenue flow and claim accuracy.