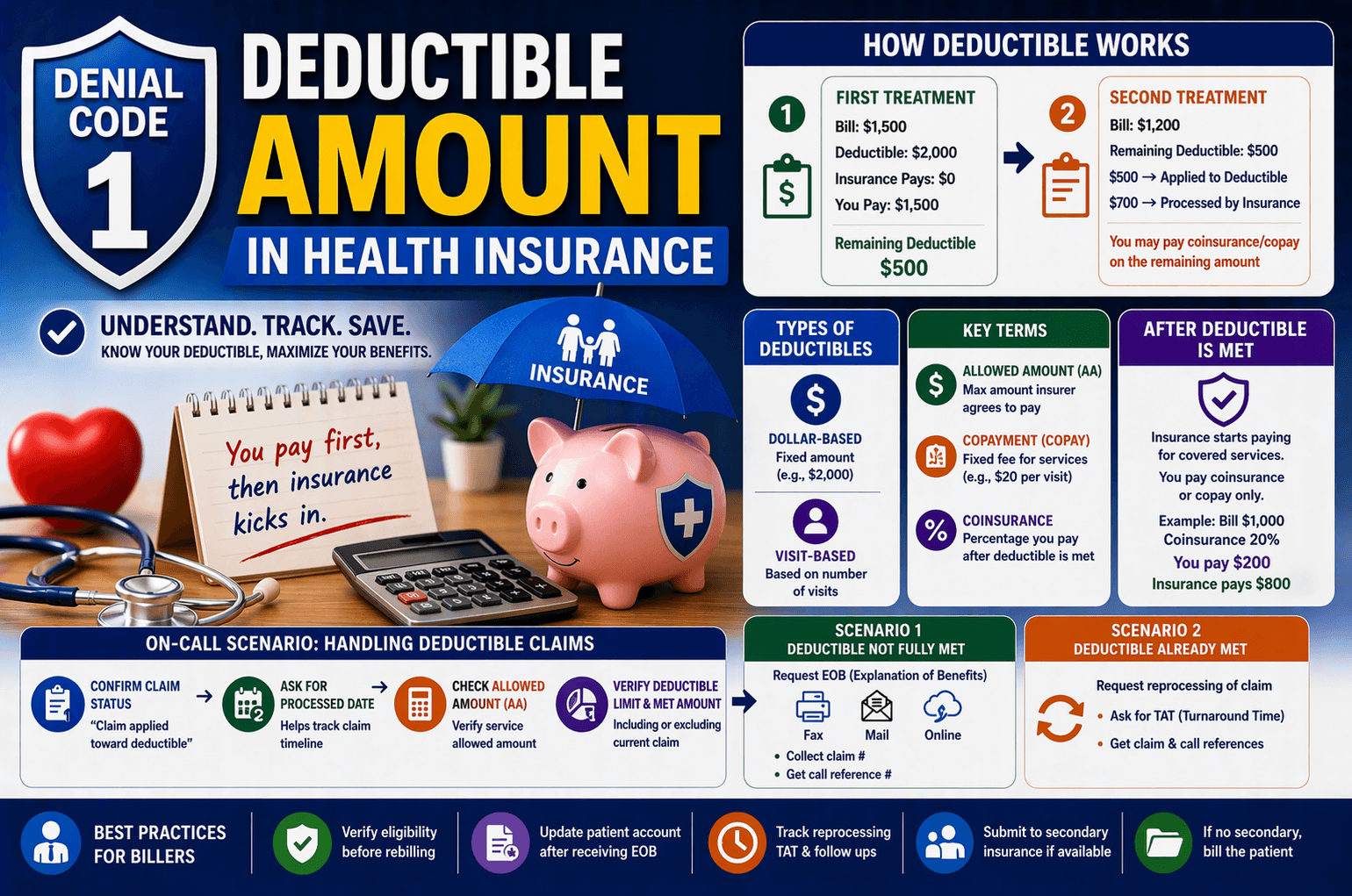

Health insurance can feel confusing, especially when terms like deductible, co-payment, and coinsurance come into play. One of the most important concepts to understand is the deductible amount—because it directly impacts how much you pay out of pocket before your insurance starts contributing. In this guide, we’ll break down the deductible in simple terms, explain how it works with real-life scenarios, and walk you through how it affects claim processing. Whether you’re new to insurance or looking to refresh your knowledge, this article will help you clearly understand the concept.

What is a Deductible Amount?

A deductible is a fixed amount that a policyholder must pay before the insurance company starts paying for medical expenses.

Simple Definition:

It’s the amount you pay first, out of your own pocket, before your insurance kicks in.

Example:

Deductible: $2,000

Medical bill: $1,500

Insurance pays: $0

You pay: $1,500 (applied toward deductible)

You still have $500 left to meet your deductible.

How Deductibles Work: Step-by-Step Example

Let’s understand this with a real scenario:

First Treatment

Treatment cost: $1,500

Deductible: $2,000

Insurance pays: $0

Patient pays: $1,500

Remaining deductible: $500

Second Treatment

Treatment cost: $1,200

Remaining deductible: $500

Now:

$500 → applied to deductible

Remaining $700 → processed by insurance

However, from this $700:

You may still pay a portion (coinsurance/copay)

Types of Deductibles

Deductibles can be structured in different ways depending on the insurance policy.

1. Dollar-Based Deductible

Fixed monetary amount (e.g., $1,000, $2,000)

Most common type

2. Visit-Based Deductible

Based on the number of visits

Example: First 3 visits fully paid by patient

After reaching the limit, insurance starts covering costs.

Key Terms You Should Know

Understanding deductibles becomes easier when you know related terms:

Allowed Amount (AA)

The maximum amount an insurer agrees to pay for a service.

Copayment (Copay)

A fixed fee you pay for services (e.g., $20 per visit).

Coinsurance

A percentage of the cost you share with the insurer after deductible is met.

On-Call Scenario: Handling Deductible Claims

When working in medical billing or insurance follow-up, here’s a typical flow when a claim is applied to a deductible:

Step-by-Step Process:

Confirm Claim Status

“Claim applied toward deductible”

Ask for Processed Date

Helps track claim timeline

Check Allowed Amount (AA)

Verify Deductible Limit

Total deductible for the policy

Check Deductible Met Amount

Including or excluding current claim

Decision Paths

Scenario 1: Deductible NOT Fully Met

Request EOB (Explanation of Benefits)

Options:

Fax

Mail

Online source

Collect:

Claim number

Call reference number

Scenario 2: Deductible Already Met

Request reprocessing of claim

Ask:

Turnaround Time (TAT)

Claim reference details

What Happens After Deductible is Met?

Once the deductible is fully met:

Insurance starts paying for covered services

Patient pays:

Coinsurance or copay only

Example:

Deductible met

Bill: $1,000

Coinsurance: 20%

You pay $200, insurance pays $800

Important Actions for Billing Professionals

If you work in healthcare billing, here are key steps to follow:

After Receiving EOB:

Update patient account

Send EOB for posting

If Claim Sent for Reprocessing:

Track TAT

Set follow-up reminders

Billing to Secondary Insurance:

Before rebilling:

Verify patient eligibility

Check active coverage on Date of Service (DOS)

If Secondary Insurance Exists:

Submit claim to secondary payer

If No Secondary Insurance:

Bill patient directly

Special Case: Medicare Claims

When dealing with Medicare:

Medicare often forwards claims to secondary payers automatically

If no response after 30 days:

Follow up with insurance

Out-of-Network Considerations

If a claim is processed as out-of-network:

Full amount may become patient responsibility

You can:

Bill secondary payer (if available)

Otherwise, bill patient directly

Key Tips to Remember

Always track how much deductible is met

Request EOB for accurate details

Verify eligibility before rebilling

Monitor reprocessing timelines

Don’t assume insurance will pay until deductible is met

Frequently Asked Questions (FAQs)

1. What happens if I never meet my deductible?

You will continue to pay for covered services out of pocket, and insurance may not contribute (except for preventive services in some plans).

2. Does deductible apply to all medical services?

Not always. Some services like preventive care may be covered without requiring you to meet the deductible.

3. Is deductible the same as out-of-pocket maximum?

No.

Deductible: Amount you pay before insurance starts

Out-of-pocket maximum: The total limit you pay in a year

4. Can I have multiple deductibles?

Yes. Some plans have:

Individual deductible

Family deductible

Separate deductibles for services (e.g., prescriptions)

5. What is an EOB and why is it important?

An Explanation of Benefits (EOB) shows:

What was billed

What insurance paid

What you owe

It’s essential for tracking deductible and payments.

Conclusion:

Understanding the deductible amount is crucial for managing both your healthcare expenses and insurance claims effectively. It determines how much you need to pay upfront and influences how your insurance benefits are applied. Whether you’re a patient trying to control costs or a billing professional handling claims, knowing how deductibles work helps you make informed decisions, avoid billing errors, and ensure accurate claim processing. Take time to review your insurance policy, track your deductible progress, and always verify details when dealing with claims—this knowledge can save you both time and money.