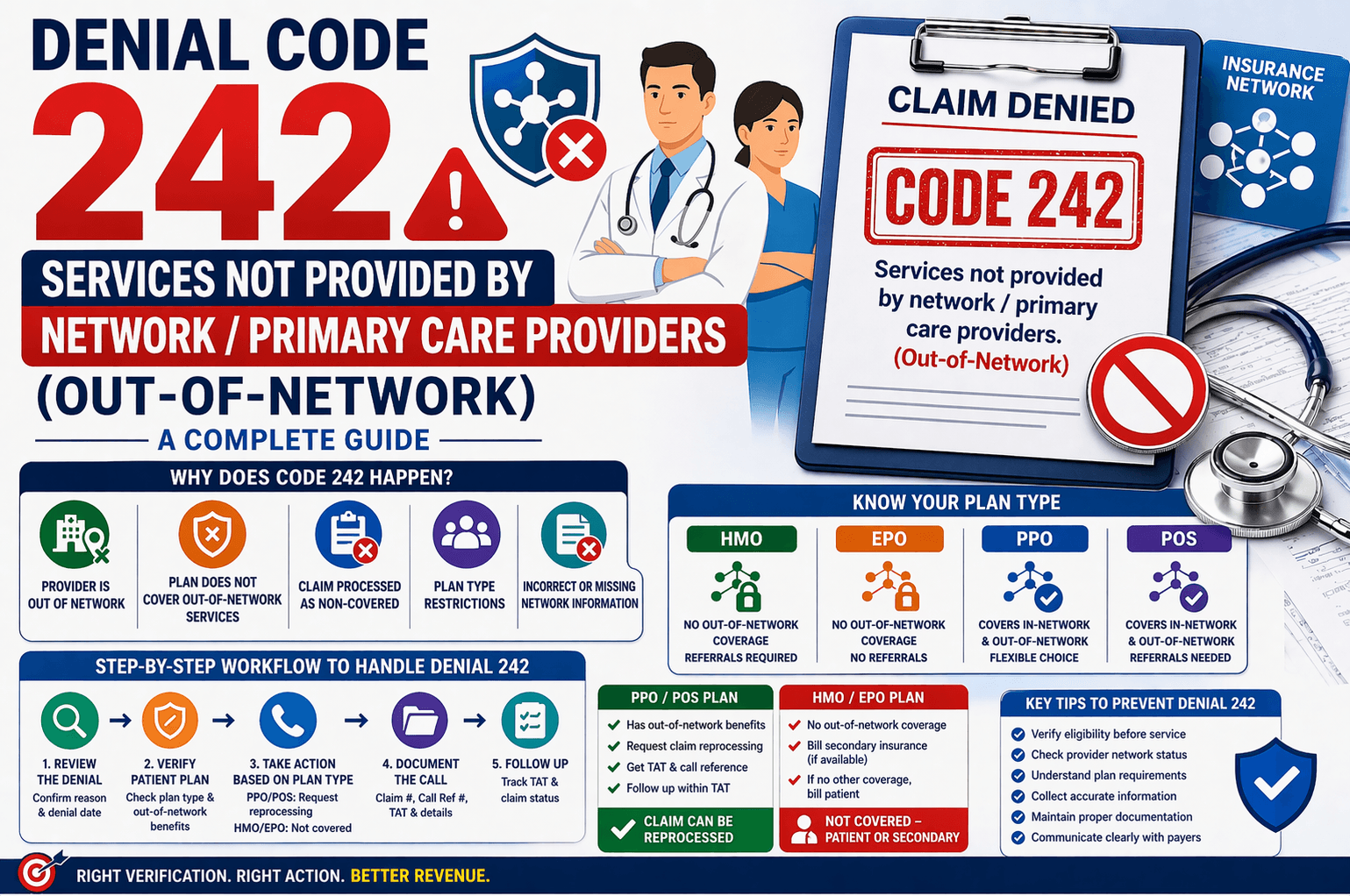

In medical billing and insurance processing, denial codes are a common part of the workflow. One such frequently encountered denial is Code 242, which indicates that services were provided by an out-of-network provider and are not covered under the patient’s insurance plan.

Understanding this denial is critical for billing professionals, revenue cycle teams, and healthcare providers. If handled correctly, it can either lead to claim reprocessing or appropriate billing to the patient or secondary payer.

This guide breaks down Denial Code 242 in simple terms, explains when it occurs, and provides actionable steps to resolve it effectively.

What Is Denial Code 242?

Denial Code 242 is issued when:

The provider is not contracted (out-of-network) with the insurance payer.

The patient’s insurance plan does not include out-of-network benefits, or the payer processes it as non-covered.

In Simple Terms:

If a patient receives care from a provider outside their insurance network, the claim may be denied unless their plan allows such services.

Why Does This Denial Occur?

There are a few key reasons behind this denial:

- Provider Is Out of Network

The healthcare provider is not part of the insurance company’s approved network. - Patient Plan Restrictions

Some plans do not cover out-of-network services at all. - Plan Type Limitations

Coverage depends heavily on the type of insurance plan:

HMO (Health Maintenance Organization) → No out-of-network coverage

EPO (Exclusive Provider Organization) → No out-of-network coverage

PPO (Preferred Provider Organization) → Covers out-of-network

POS (Point of Service) → Covers out-of-network

Understanding Insurance Plan Types

Knowing the patient’s plan is essential to resolve Denial 242 correctly.

HMO Plans

Strict network rules

No coverage outside the network

Requires referrals for specialists

EPO Plans

Similar to HMO

No out-of-network benefits

PPO Plans

Flexible provider choice

Covers both in-network and out-of-network services

Higher cost for out-of-network

POS Plans

Hybrid model

Allows out-of-network coverage with referrals

Step-by-Step Workflow to Handle Denial 242

Here’s a structured approach to manage this denial efficiently:

Step 1: Review the Denial

Confirm denial reason: “Non-covered services – provider out of network”

Note the denial date

Step 2: Verify Patient Plan

Ask:

Does the plan include out-of-network benefits?

What is the plan type (HMO, PPO, EPO, POS)?

Step 3: Take Action Based on Plan Type

If PPO or POS:

Contact payer and request:

Claim reprocessing

Ask:

“Since the patient has out-of-network benefits, can you reprocess the claim?”

Record:

Call reference number

Claim number

TAT (Turnaround Time)

If HMO or EPO:

Out-of-network services are not covered

Proceed with:

Billing to secondary insurance (if available)

Or patient responsibility

On-Call Scenario (Practical Approach)

When calling the insurance representative, follow this flow:

Confirm denial reason

Ask for denial date

Verify out-of-network coverage

Identify plan type

Take appropriate action:

For PPO/POS:

Request reprocessing

Ask for TAT

Document call details

For HMO/EPO:

Collect claim and reference details

Move claim to next billing step

Key Actions to Take

If Claim Can Be Reprocessed:

Follow up within the TAT provided

Track claim status regularly

If Claim Cannot Be Reprocessed:

Check for secondary or consecutive payer

Verify eligibility before billing

If No Other Coverage:

Release claim to patient billing

Important Tips for Billing Teams

Always verify eligibility before submission

Prevents unnecessary denials

Check provider network status in advance

Avoids out-of-network surprises

Document every call with payer

Helps during audits or escalations

Understand plan types thoroughly

Reduces errors in claim handling

Set timely follow-ups

Ensures faster revenue recovery

Example Scenario

Case:

A patient with a PPO plan receives treatment from an out-of-network provider.

Outcome:

Claim initially denied (Code 242)

Billing team contacts payer

Confirms PPO includes out-of-network benefits

Requests reprocessing

Claim gets approved after review

FAQs

- What does Denial Code 242 mean?

It means the service was provided by an out-of-network provider and is not covered under the patient’s plan. - Can Denial 242 be overturned?

Yes, if the patient has PPO or POS coverage, the claim can often be reprocessed. - What should be done for HMO or EPO plans?

Since they don’t cover out-of-network services:

Bill secondary insurance (if available)

Otherwise, bill the patient - Why is eligibility verification important?

It helps confirm:

Plan type

Coverage details

Prevents avoidable denials - What is TAT in claim reprocessing?

TAT (Turnaround Time) is the time the payer takes to reprocess the claim after request.

Conclusion:

Denial Code 242 is a common but manageable issue in medical billing. The key to resolving it lies in understanding insurance plan types, verifying out-of-network benefits, and following a structured workflow.

For PPO and POS plans, reprocessing is often possible, while HMO and EPO plans require shifting responsibility to secondary payers or patients. By applying the right steps and maintaining proper documentation, billing teams can minimize revenue loss and improve claim success rates.

A proactive approach—especially eligibility verification and network checks—can significantly reduce the occurrence of this denial in the first place.