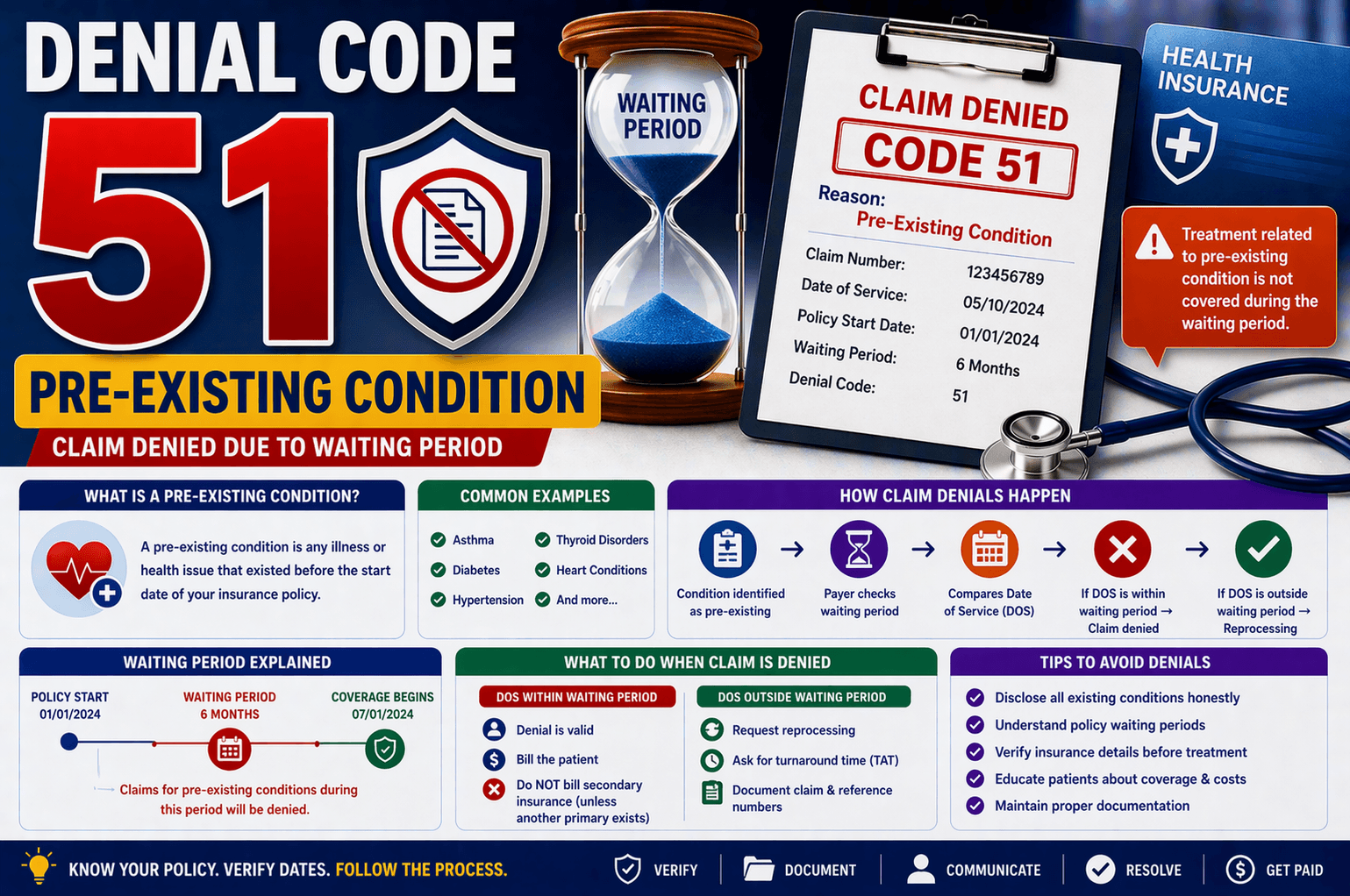

Health insurance is meant to protect individuals from unexpected medical expenses. However, not all claims are approved. One common reason for claim denial is a pre-existing condition. If you’ve ever heard your claim was denied because of this, you might have found it confusing or frustrating.

In simple terms, a pre-existing condition is any illness or health issue a person already has before purchasing a new insurance policy. Insurance companies often apply special rules to such conditions, which can lead to claim denials—especially during the waiting period.

This article breaks down everything you need to know about pre-existing condition denials, including how they work, why they happen, and what actions you can take.

What Is a Pre-Existing Condition?

A pre-existing condition refers to any medical condition that existed before the start date of your insurance policy.

Common Examples:

Asthma

Diabetes

Hypertension

Thyroid disorders

Heart conditions

Insurance companies consider these conditions high-risk because the chances of filing claims related to them are higher.

Why Do Insurance Companies Deny These Claims?

Insurance providers use a concept called a waiting period for pre-existing conditions. This is a specific duration during which the insurance policy will not cover claims related to that condition.

Key Reasons for Denial:

The illness existed before policy purchase

The claim was filed during the waiting period

The condition was not disclosed during policy enrollment

Example:

Imagine a person with asthma buys a new health insurance policy. If the policy includes a 6-month waiting period for pre-existing conditions, any asthma-related claims during those 6 months will be denied.

Understanding the Waiting Period

The waiting period is a crucial concept in insurance policies.

What Does It Mean?

It is the time you must wait after your policy starts before you can claim benefits for certain conditions—especially pre-existing ones.

Key Points:

Typically ranges from 6 months to 4 years

Starts from the policy’s effective date

Applies only to specific conditions

Example Breakdown:

Policy start date: January 1

Waiting period: 6 months

Coverage begins: July 1

If a claim is filed between January and June for a pre-existing condition, it will be denied.

How Claim Denials Happen (Real Scenario)

Let’s walk through a typical scenario to understand how this works in practice:

Situation:

A claim is denied because it is marked as a non-covered service due to a pre-existing condition.

Step-by-Step Process:

The insurance company identifies the condition as pre-existing

They check the policy’s waiting period

They compare the Date of Service (DOS) with the waiting period timeline

Decision Path:

If DOS falls within the waiting period → Claim denied

If DOS falls outside the waiting period → Claim should be reprocessed

What to Do When a Claim Is Denied

If you’re handling a denied claim (as a patient, billing specialist, or healthcare provider), follow this structured approach:

- Verify the Denial Details

Ask for the denial date

Confirm the reason mentioned - Check Waiting Period Dates

Identify the start and end dates of the waiting period

Compare with the Date of Service (DOS) - Take Action Based on Findings

If DOS is within the waiting period:

The denial is valid

Bill the patient directly

Do not send to secondary insurance (unless another primary exists)

If DOS is outside the waiting period:

Request claim reprocessing

Ask for turnaround time (TAT)

Document claim number and reference number

Important Billing Guidelines

When dealing with pre-existing condition denials, proper billing practices are essential.

Follow These Rules:

Bill the patient if the claim falls within the waiting period

Bill another primary insurance if available

Do NOT bill secondary insurance if the primary denies due to pre-existing condition

Always document claim reference details

Tips to Avoid Claim Denials

Preventing denials is always better than fixing them later. Here are some practical tips:

For Patients:

Disclose all existing health conditions honestly

Read policy terms carefully before buying

Understand waiting periods clearly

For Healthcare Providers:

Verify insurance details before treatment

Check policy coverage for pre-existing conditions

Educate patients about possible out-of-pocket costs

For Billing Teams:

Always verify DOS vs waiting period

Maintain proper documentation

Follow up on reprocessing requests promptly

Frequently Asked Questions (FAQs)

- What is the most common reason for pre-existing condition denial?

The most common reason is filing a claim during the waiting period specified in the policy. - Can insurance companies permanently deny coverage for pre-existing conditions?

Not always. Many insurers cover them after the waiting period ends, but some may charge higher premiums. - What happens if I didn’t disclose my condition while buying insurance?

Non-disclosure can lead to claim rejection or even policy cancellation. Always provide accurate information. - Can I appeal a denied claim?

Yes, especially if the denial was incorrect. For example, if the Date of Service is outside the waiting period, you can request reprocessing. - Should I bill secondary insurance after denial?

No, not if the denial is due to a pre-existing condition. Secondary insurers usually won’t process such claims.

Conclusion:

Pre-existing condition denials are a common but manageable part of health insurance. Understanding how waiting periods work and how insurers evaluate claims can save you time, money, and frustration.

The key takeaway is simple: timing matters. If your claim falls within the waiting period, it will likely be denied. But if it falls outside, you have every right to request reprocessing.

By staying informed, verifying policy details, and following proper procedures, you can handle these situations confidently and avoid unnecessary complications.

Whether you are a patient, healthcare provider, or billing professional, a clear understanding of pre-existing condition rules will help you navigate the insurance process more effectively.