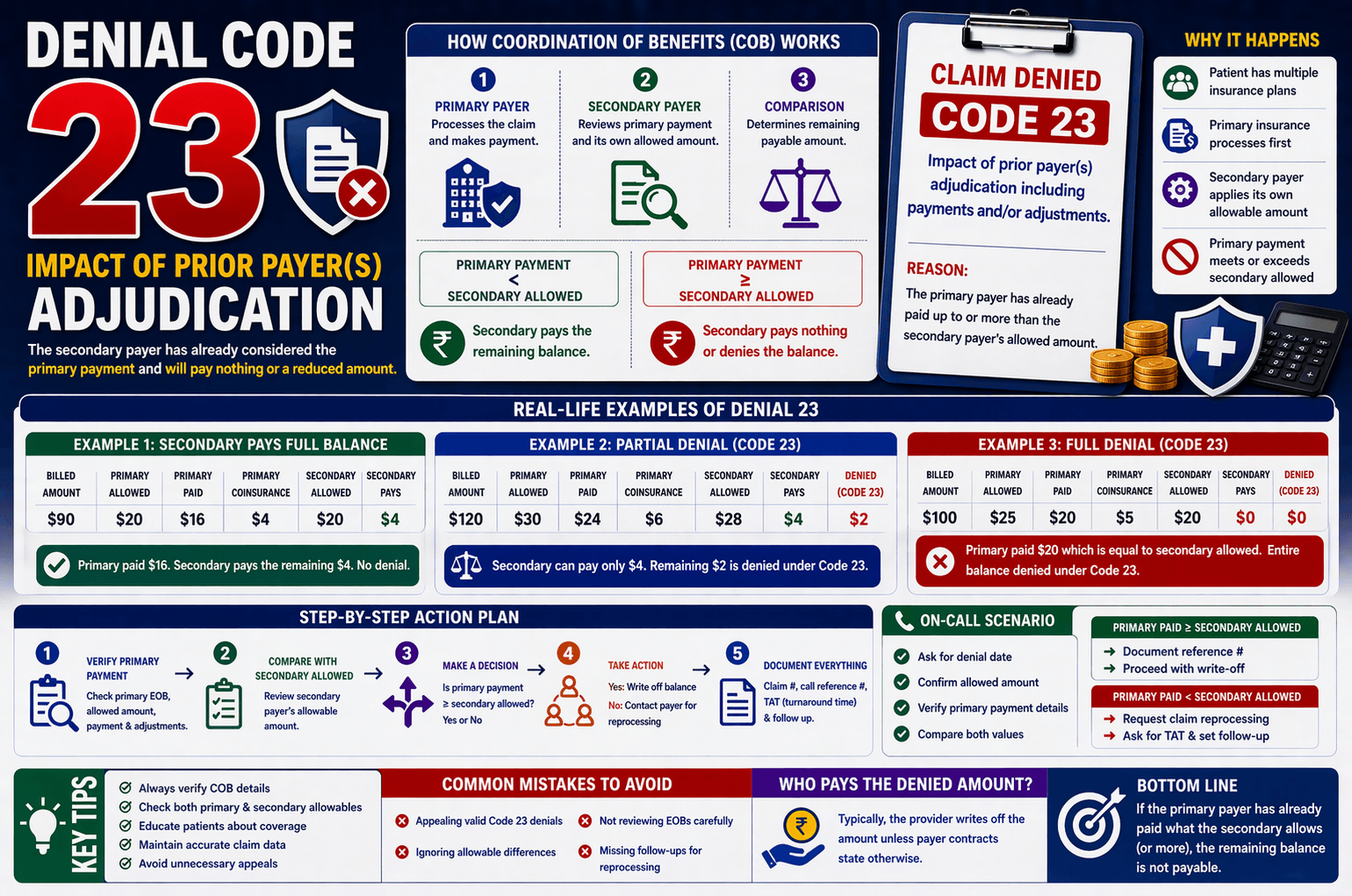

In medical billing, denial codes can be confusing—especially for beginners. One of the most common yet misunderstood codes is Denial Code 23, which refers to “the impact of prior payer(s) adjudication including payments and/or adjustments.”

Simply put, this denial happens when the primary insurance has already paid enough—or more than what the secondary insurance allows. As a result, the secondary payer either pays a reduced amount or denies the remaining balance altogether.

Understanding this denial is critical for revenue cycle management professionals, as it directly impacts reimbursement and write-offs. This guide breaks down Denial 23 in a clear, beginner-friendly way with practical examples and actionable tips.

What Is Denial Code 23?

Denial Code 23 occurs during coordination of benefits (COB) when:

A patient has more than one insurance plan

The primary insurance processes the claim first

The secondary insurance reviews what the primary has already paid

If the primary payment is equal to or greater than the secondary allowable amount, the secondary payer will:

Pay nothing, or

Pay only a small remaining balance

This leads to a denial or partial denial under Code 23.

How Coordination of Benefits Works

Before diving deeper, let’s understand the process:

Primary Insurance Pays First

The claim is processed, and payment is made based on their allowed amount.

Secondary Insurance Reviews the Claim

It considers:

What the primary paid

Its own allowed amount

Comparison Happens

If primary payment ≥ secondary allowed → denial or no payment

If primary payment < secondary allowed → partial payment

Real-Life Examples of Denial 23

Example 1: Full Secondary Payment

Billed Amount: $90

Primary Allowed: $20

Primary Paid: $16

Coinsurance (Patient Responsibility): $4

Secondary Allowed: $20

Since primary paid $16, the secondary pays the remaining $4.

Result: No denial—secondary covers the balance.

Example 2: Partial Denial

Billed Amount: $120

Primary Allowed: $30

Primary Paid: $24

Coinsurance: $6

Secondary Allowed: $28

Primary paid: $24

Secondary allowed: $28

Remaining payable: $4

The leftover $2 is denied under Code 23.

Result: Partial payment + partial denial.

Example 3: Full Denial

Billed Amount: $100

Primary Allowed: $25

Primary Paid: $20

Coinsurance: $5

Secondary Allowed: $20

Since primary already paid $20 (equal to secondary allowed):

Result: Entire remaining balance denied under Code 23.

Why Denial 23 Happens

Denial 23 is not an error—it’s usually contractual logic based on payer rules. Common causes include:

Secondary payer has lower allowable rates

Incorrect expectations of secondary coverage

Misinterpretation of coinsurance or patient responsibility

Lack of understanding of payer contracts

What to Do When You Receive Denial 23

Handling Denial 23 correctly can save time and prevent unnecessary appeals.

Step-by-Step Action Plan

- Verify Primary Payment

Check how much the primary insurance paid

Confirm allowed amount and adjustments - Compare with Secondary Allowed

Review secondary payer’s allowable amount - Make a Decision

If primary paid ≥ secondary allowed:

Write off the remaining balance

No further action needed

If primary paid < secondary allowed:

Contact secondary insurance

Request reprocessing if applicable

On-Call Scenario: How to Handle with Insurance

When calling insurance, follow a structured approach:

Ask for denial date

Confirm allowed amount

Verify primary payment details

Compare both values

Possible Outcomes:

If Primary Paid More or Equal

Document claim number and call reference

Proceed with write-off

If Primary Paid Less

Request claim reprocessing

Ask for Turnaround Time (TAT)

Set follow-up reminder

Key Tips to Avoid Denial 23 Issues

Always verify Coordination of Benefits (COB) details

Check both primary and secondary allowable amounts

Educate patients about coverage limitations

Maintain accurate billing and claim submission data

Avoid unnecessary appeals—this denial is often valid

Common Mistakes to Avoid

Appealing valid Denial 23 cases

Ignoring payer-specific allowable differences

Not reviewing Explanation of Benefits (EOB) carefully

Missing follow-ups when reprocessing is possible

Frequently Asked Questions (FAQs)

- Is Denial Code 23 always valid?

Yes, in most cases. It reflects payer coordination rules rather than billing errors. However, verification is still necessary. - Can Denial 23 be appealed?

Only if there is a processing error. If the denial is due to correct COB logic, appeals are usually not successful. - Who is responsible for the denied amount?

Typically, the provider writes off the amount, unless specified otherwise by payer contracts. - What if primary insurance paid incorrectly?

In that case:

Contact primary payer

Request correction

Then resubmit to secondary - How can I prevent Denial 23?

Ensure accurate COB information

Verify payer contracts

Review claims before submission

Conclusion:

Denial Code 23 may seem complex at first, but it becomes straightforward once you understand how primary and secondary insurance interact. The key takeaway is simple:

If the primary payer has already met or exceeded what the secondary allows, the remaining balance is not payable.

For billing professionals, the focus should be on verification, correct interpretation, and efficient handling rather than unnecessary appeals. By mastering this denial, you can improve claim resolution speed and maintain a healthy revenue cycle.

Understanding Denial 23 isn’t just about fixing claims—it’s about working smarter with payer systems.