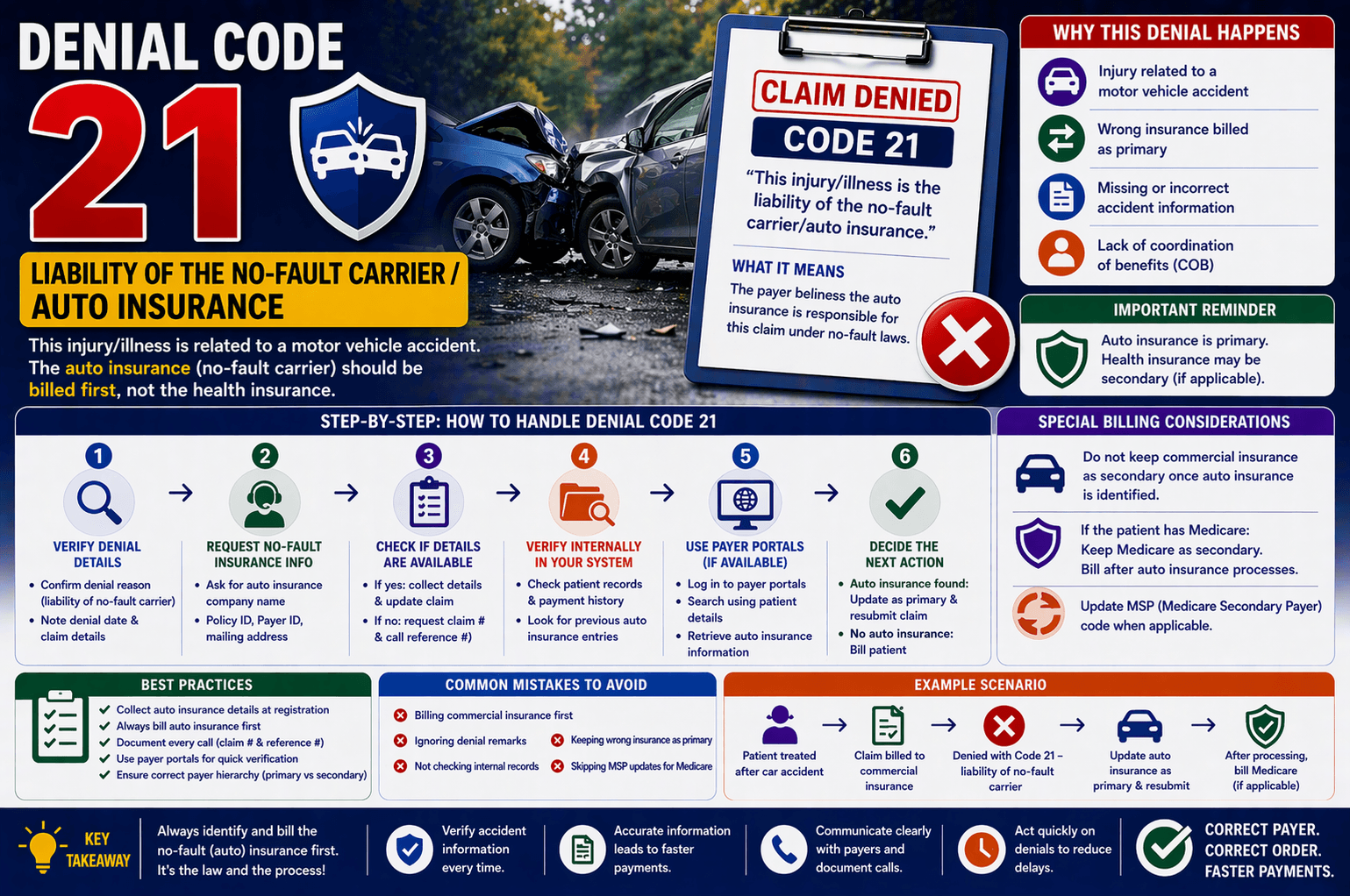

In medical billing, claim denials are a common challenge—but some can be particularly confusing, especially for beginners. One such denial reads: “This injury/illness is the liability of the no-fault carrier/auto insurance.”

If you’ve encountered this message, it means the insurance company is indicating that the treatment is related to an auto accident, and therefore, the auto insurance (no-fault carrier) should be billed instead of the commercial or primary health insurance.

Understanding how to handle this situation properly is essential for reducing delays, preventing revenue loss, and ensuring accurate claim processing. This guide breaks down everything you need to know in a simple, practical way.

What Is a No-Fault Insurance Denial?

A no-fault insurance denial occurs when a health insurance payer refuses a claim because the injury is related to a motor vehicle accident. In such cases:

Auto insurance becomes the primary payer

Health insurance may act as secondary payer (if applicable)

The provider must bill the no-fault carrier first

This type of denial is not a rejection of services—it’s simply a redirection to the correct payer.

Why Do These Denials Happen?

These denials typically occur due to:

Missing or incorrect accident information

Failure to list auto insurance as primary payer

Lack of coordination of benefits (COB)

Incomplete patient insurance details

Incorrect billing sequence

Step-by-Step Process to Handle No-Fault Denials

Let’s walk through the correct workflow to resolve this denial efficiently.

- Verify the Denial Details

Start by confirming:

Denial reason: “Liability of no-fault carrier”

Date of denial

Claim details

Why this matters: Ensures you’re working on the correct issue and claim. - Request No-Fault Insurance Information

Contact the insurance representative and ask:

Name of the auto insurance company

Policy ID

Payer ID

Mailing address

If the representative has the details, proceed to update the claim. - Check If Details Are Available

If YES:

Collect all required insurance information

Update system with auto insurance as primary

Resubmit the claim to the no-fault carrier

If NO:

Ask for:

Claim number

Call reference number

Then proceed to internal verification. - Verify Internally in Your System

If the representative cannot provide details:

Check patient records for:

Previous auto insurance entries

Payment history

Look for any indication that auto insurance was previously billed - Use Payer Portals

If access is available:

Log into payer portals

Search using patient details

Retrieve auto insurance information

This can often save time and reduce back-and-forth calls. - Decide the Next Action

Based on findings:

Scenario A: Auto Insurance Found

Update it as primary payer

Resubmit the claim

Scenario B: No Auto Insurance Found

Release the claim to patient responsibility

Special Billing Considerations

- Do Not Keep Commercial Insurance as Secondary

Once auto insurance is identified:

It must be billed as primary

Commercial insurance should not remain secondary unless appropriate coordination exists - Medicare as Secondary Payer

If the patient has Medicare:

Keep Medicare as secondary

After auto insurance processes the claim:

If balance remains → bill Medicare

Update MSP (Medicare Secondary Payer) code

Example Scenario

Let’s simplify with an example:

Situation:

A patient visits a clinic after a car accident. The claim is mistakenly billed to commercial insurance.

Outcome:

Commercial payer denies with “liability of no-fault carrier.”

Resolution:

Contact payer → request auto insurance details

Update system → auto insurance as primary

Resubmit claim

After processing → bill Medicare (if applicable)

Key Tips for Handling No-Fault Denials

Always verify accident-related cases during patient registration

Collect auto insurance details upfront

Document every call (claim # and reference #)

Use payer portals whenever possible

Ensure correct payer hierarchy (primary vs secondary)

Avoid unnecessary delays by acting immediately on denials

Common Mistakes to Avoid

Billing commercial insurance first

Ignoring denial remarks

Not checking internal records

Keeping wrong insurance as primary

Skipping MSP updates for Medicare

Frequently Asked Questions (FAQs)

- What does “no-fault carrier” mean in medical billing?

It refers to auto insurance that covers medical expenses regardless of who caused the accident. - Can I bill health insurance before auto insurance?

No. Auto insurance must always be billed first if the injury is accident-related. - What if no auto insurance information is available?

You should:

Check internal systems

Review patient history

If still unavailable → bill the patient - Is Medicare always secondary in these cases?

Yes, if auto insurance exists. Medicare becomes secondary and is billed after the primary payer processes the claim. - Why is my claim denied even though I submitted it correctly?

Possible reasons include:

Missing accident indicator

Incorrect payer sequence

Lack of coordination of benefits

Conclusion

Handling no-fault insurance denials may seem complex at first, but once you understand the workflow, it becomes manageable. The key is to identify the correct payer, gather accurate information, and follow proper billing hierarchy.

By verifying denial details, collecting auto insurance data, and updating claims correctly, you can significantly reduce delays and improve claim success rates.

For beginners in medical billing, mastering this process is an essential step toward becoming efficient and error-free in claims management.