Author_Hendry")

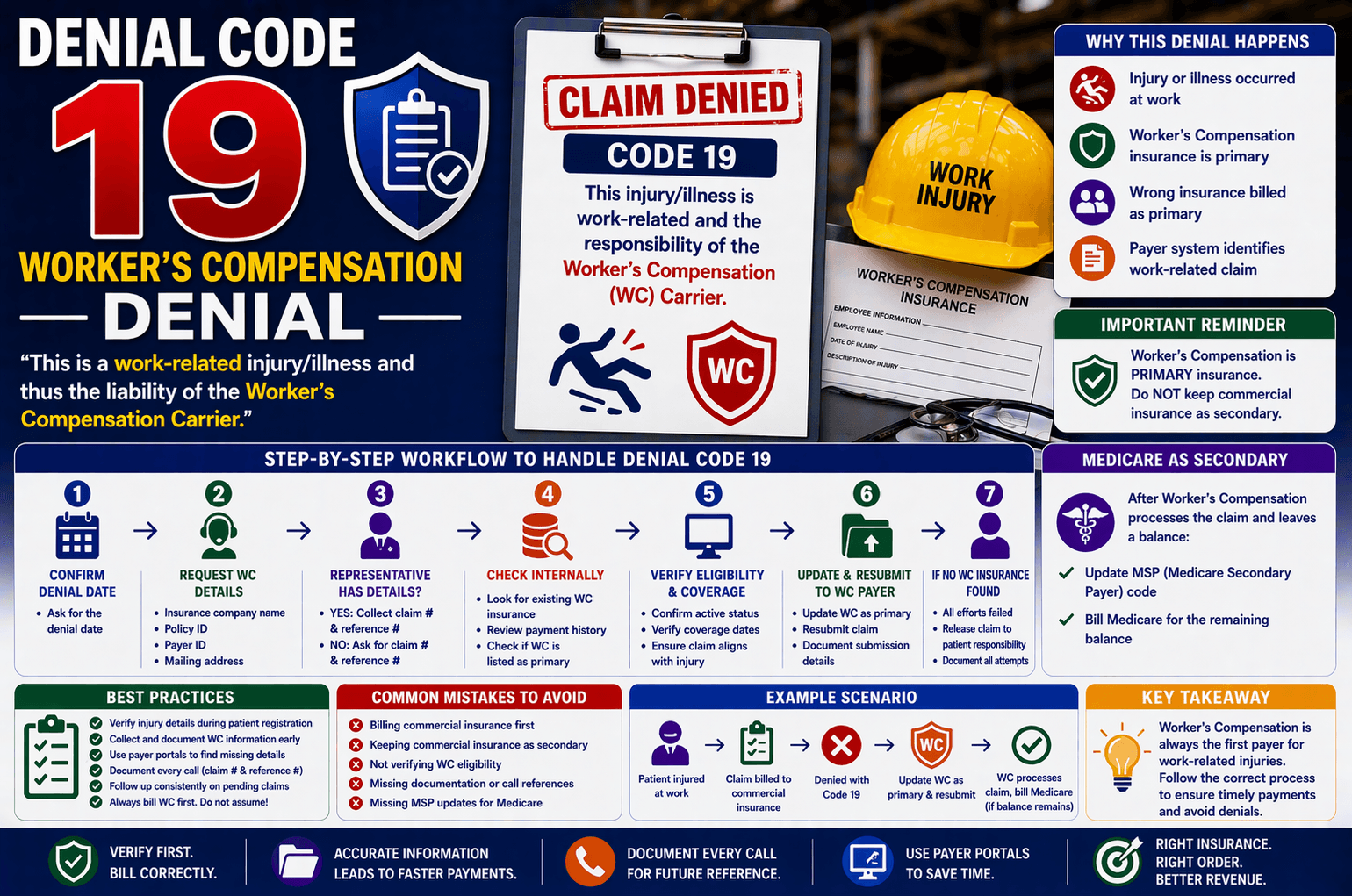

In medical billing, claim denials are common—but understanding why a claim is denied is critical to resolving it efficiently. One such denial scenario is when a claim is rejected because the injury or illness is work-related, making it the responsibility of the Worker’s Compensation (WC) carrier, not the regular health insurance payer.

This article breaks down the workflow, decision-making process, and best practices for handling such denials. Whether you’re new to medical billing or looking to sharpen your skills, this guide will help you navigate Worker’s Compensation cases with clarity and confidence.

What Does This Denial Mean?

When a payer denies a claim stating:

“This is a work-related injury/illness and thus the liability of the Worker’s Compensation Carrier”

…it indicates that the treatment provided is linked to a workplace incident. Therefore, the billing responsibility shifts from commercial or private insurance to the Worker’s Compensation insurance provider.

Step-by-Step Workflow to Handle the Denial

Handling this denial requires a structured approach. Below is a simplified workflow used in real-world billing scenarios.

- Confirm the Denial Date

Start by asking:

“May I get the denial date?”

This helps track timelines and ensures compliance with filing deadlines. - Request Worker’s Compensation Details

Next, gather essential information:

Name of the WC insurance company

Policy ID

Payer ID

Mailing address

Ask clearly:

“Could you please provide the worker compensation details?” - Check if the Representative Has the Details

This step determines your next move:

✔ If YES (Details Available)

Proceed to collect:

Claim number

Call reference number

Then:

Update the WC insurance as primary insurance

Resubmit the claim to the WC payer

✖ If NO (Details Not Available)

Ask:

“May I have the claim number and call reference number?”

Then move to internal verification steps (explained below).

What to Do If WC Details Are Missing

Sometimes, the insurance representative doesn’t have Worker’s Compensation information. In such cases:

Check Internal Systems

Look for:

Existing WC insurance records

Patient payment history

Any indication of WC as primary insurance

Verify Eligibility

If WC insurance is found:

Check eligibility status

Confirm coverage dates

Ensure claim aligns with the injury

Resubmit the Claim

If valid WC insurance exists:

Update it as primary insurance

Submit the claim to the WC payer

If No WC Insurance Is Found

If all checks fail:

Release the claim to the patient

Document all efforts made

Using Payer Portals for WC Information

Many payer portals provide additional insights. If you have access:

Search for WC-related claims

Look for accident-related notes

Retrieve missing insurance details

This step can save time and prevent unnecessary delays.

Coordination of Benefits (COB): Important Rules

Handling multiple insurances requires attention to hierarchy.

Key Guidelines:

Worker’s Compensation = Primary Insurance

Do NOT keep commercial insurance as secondary

Medicare CAN be secondary

When Medicare Is Secondary

If WC processes the claim but leaves a balance:

Update the MSP (Medicare Secondary Payer) code

Bill Medicare for the remaining amount

Common Mistakes to Avoid

Avoid these frequent errors:

Billing commercial insurance before WC

Not verifying WC eligibility

Missing claim resubmission deadlines

Keeping incorrect insurance order

Failing to document calls and references

Practical Example

Scenario:

A patient visits for a back injury. The claim is sent to commercial insurance and gets denied as work-related.

Correct Action:

Confirm denial reason and date

Ask for WC details

Check system for existing WC policy

Update WC as primary

Resubmit claim to WC payer

If WC pays partially, bill Medicare (if applicable).

Key Tips for Efficient Handling

Always verify injury cause at registration

Maintain clear documentation of all calls

Use payer portals whenever possible

Follow up consistently on pending WC claims

Train staff to identify work-related cases early

Frequently Asked Questions (FAQs)

- What is Worker’s Compensation in medical billing?

Worker’s Compensation is insurance that covers medical expenses for injuries or illnesses that occur due to work-related activities. - Why was my claim denied as work-related?

The payer determined that the treatment is linked to a workplace injury, making WC insurance responsible instead of regular health insurance. - Can I bill both WC and commercial insurance?

No. WC must always be billed as primary. Commercial insurance should not be billed unless WC denies liability. - What if WC insurance details are unavailable?

Check internal systems, patient history, and payer portals. If no information is found, the claim may be transferred to patient responsibility. - When can Medicare be billed?

Medicare can be billed as secondary after WC processes the claim and leaves a remaining balance.

Conclusion:

Handling Worker’s Compensation denials may seem complex at first, but with a structured approach, it becomes manageable. The key lies in accurate information gathering, proper insurance sequencing, and timely claim resubmission.

By following the workflow outlined in this guide, you can reduce denials, improve reimbursement rates, and ensure compliance with billing regulations. Mastering this process is an essential skill for anyone working in medical billing and revenue cycle management.