Retirement planning is often ignored by people who work in small shops, farms, daily-wage jobs, home-based businesses, or informal services. Many of them earn regularly during their working years but do not have a fixed pension after old age. The Atal Pension Yojana (APY) was created to address this gap by encouraging small, regular savings for retirement. It is a government-backed pension scheme focused mainly on workers in the unorganised sector.

Main Content

What Is Atal Pension Yojana?

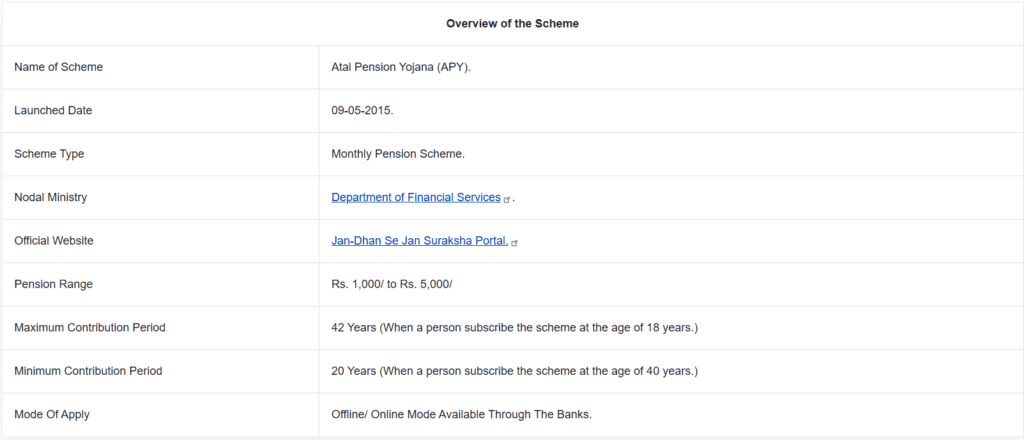

Atal Pension Yojana is a voluntary pension scheme launched in 2015 and implemented from June 1, 2015. It aims to provide old-age income security, especially for poor, underprivileged, and unorganised-sector workers.

Under APY, a subscriber contributes a fixed amount regularly until the age of 60. After that, the subscriber receives a guaranteed monthly pension of ₹1,000, ₹2,000, ₹3,000, ₹4,000, or ₹5,000, depending on the pension option selected and the contribution made.

Who Can Join APY?

Eligibility Rules

APY is available to Indian citizens who have a savings bank account in a bank or Department of Posts. The joining age is from 18 years to 40 years. From October 1, 2022, a person who is or has been an income-tax payer is not eligible to join the scheme.

This rule makes APY more focused on citizens who need basic pension support but may not have access to formal retirement benefits.

How Contributions Work

Small Payments, Long-Term Benefit

The contribution amount depends on three factors: the subscriber’s age, the pension amount chosen, and the payment frequency. A younger person pays less because the contribution period is longer. For example, an 18-year-old pays much less for the ₹5,000 pension option than a person joining at age 40. The official APY contribution chart shows monthly, quarterly, and half-yearly options for different entry ages and pension levels.

Contributions are usually made through auto-debit from the subscriber’s bank account. This makes saving easier because the amount is deducted automatically at the chosen interval.

Benefits of Atal Pension Yojana

Guaranteed Pension After 60

The biggest benefit of APY is the government-guaranteed minimum pension after the age of 60. This gives subscribers some financial stability during old age, especially when regular income may stop.

Support for Spouse and Nominee

APY also gives family protection. After the subscriber’s death, the spouse is entitled to receive the same pension amount. After the death of both subscriber and spouse, the nominee receives the accumulated pension wealth.

Useful for Informal Workers

APY is especially useful for people who do not have employer-provided pensions, provident fund benefits, or organised-sector retirement plans. Street vendors, drivers, domestic workers, small farmers, shop helpers, and self-employed workers can use it as a simple retirement tool.

Why APY Matters in Current Affairs

India’s pension system is becoming more important because people are living longer and work patterns are changing. Many workers today do not remain in one formal job for life. APY helps expand pension coverage beyond government employees and organised-sector workers.

According to a 2026 Press Information Bureau update, APY reached 8.96 crore enrolments as of March 31, 2026, showing its growing role in India’s social security system.

Practical Tips

Choose the Pension Amount Carefully

Do not choose only the lowest contribution option. Think about future expenses such as food, medicines, rent, and family support. A higher pension option may be better if your income allows it.

Keep Enough Balance in the Bank Account

Since APY uses auto-debit, subscribers should maintain enough balance before the deduction date. Missed contributions can create penalties and may disturb long-term savings.

Update Nominee and Bank Details

Subscribers should keep nominee, mobile number, Aadhaar, and bank details updated. This helps avoid problems later during pension claims or family benefit settlement.

Key Takeaways

Atal Pension Yojana is a government-backed pension scheme for long-term old-age income support.

It is open to eligible Indian citizens aged 18 to 40 with a savings bank or post office account.

The pension starts after 60 and ranges from ₹1,000 to ₹5,000 per month.

The scheme also provides spouse pension and nominee benefits.

Conclusion

Atal Pension Yojana is not a luxury investment plan; it is a practical social security tool for people who may not have any other pension support. Its strength lies in simple contributions, guaranteed pension benefits, and family protection. For young workers in the informal sector, joining early can make retirement planning more affordable. As India’s workforce continues to change, APY remains an important step toward financial dignity in old age.