Author_Hendry")

Claim Denied: “This Injury/Illness is the Liability of the No-Fault Carrier” – What to Do?

When working on medical billing and denial management, one common denial is:

“This injury/illness is the liability of the No-Fault carrier / Auto insurance.”

This denial usually means the payer is saying the medical services were related to an auto accident (MVA – Motor Vehicle Accident), and the claim should be billed to the No-Fault/Auto insurance, not the commercial insurance.

In this guide, we will explain the exact call flow and steps to resolve this denial quickly.

What Does This Denial Mean?

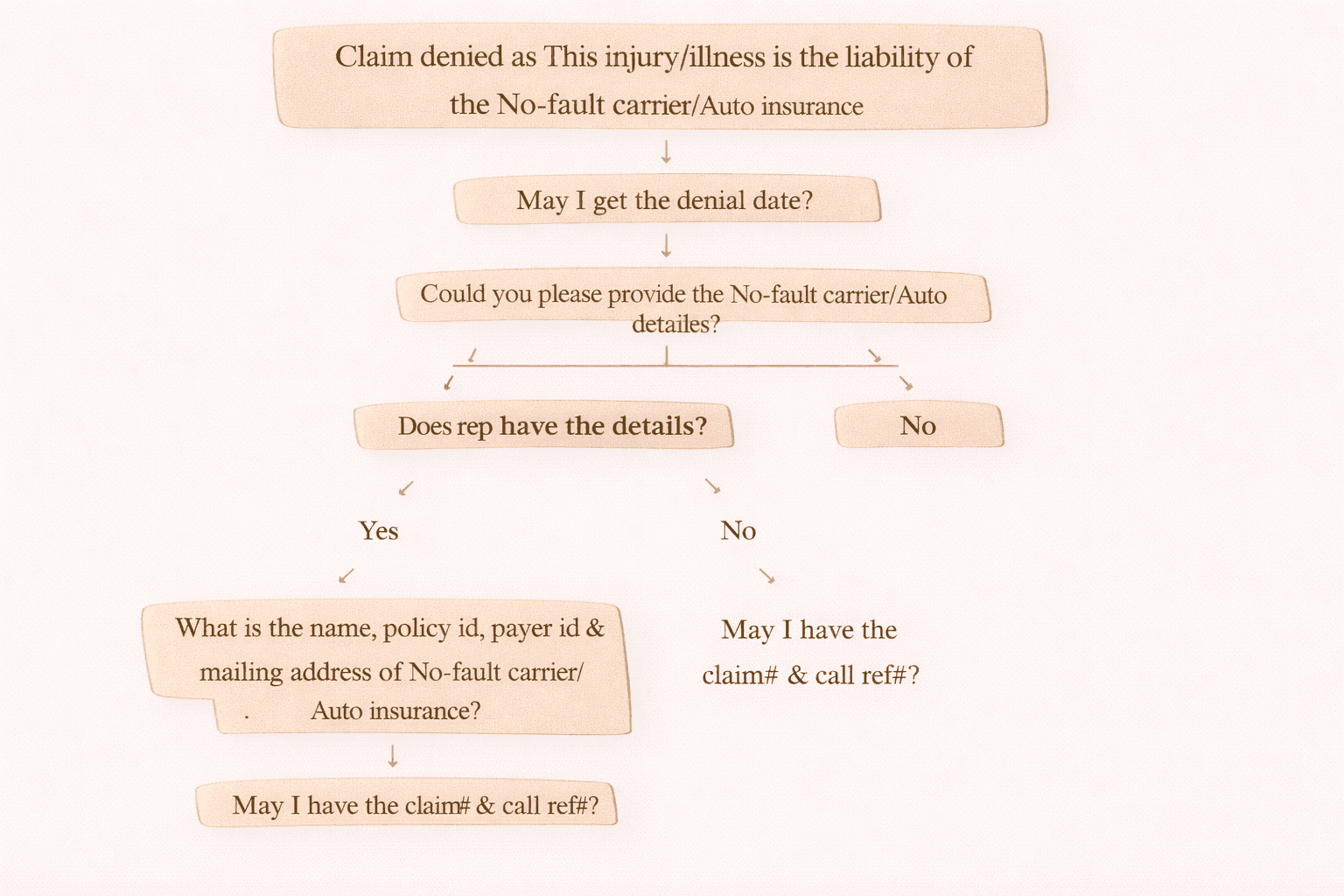

If a claim is denied with:

“This injury/illness is the liability of the No-Fault carrier”

It means:

• The patient’s treatment is accident-related

• The primary responsibility is Auto/No-Fault insurance

• The claim must be billed to the correct payer

On-Call Denial Handling Workflow (Step-by-Step)

Step 1: Confirm Denial Date

Start the call politely and professionally:

“May I get the denial date?”

This is important for:

• timely filing tracking

• appeal windows

• next action planning

Step 2: Ask for Auto / No-Fault Insurance Information

“Could you please provide the No-fault carrier / Auto insurance details?”

Does the Representative Have Auto Insurance Details?

Scenario A: YES, Rep Has Details

If rep confirms they have No-Fault carrier info, collect the full details:

Ask:

“What is the name, policy ID, payer ID, and mailing address of the No-Fault carrier/Auto insurance?”

Then request tracking info:

“May I have the claim number and call reference number?”

Scenario B: NO, Rep Does NOT Have Details

If the rep does not have No-Fault insurance details, collect identifiers:

“May I have the claim number & call reference number?”

Then proceed with internal research.

Important Note: What to Do if No-Fault Info is Not Available

If the rep does not provide No-Fault details, then you must do the following checks:

1) Check Internal System

Look for:

• any Auto/No-Fault insurance under patient insurance

• patient’s payment history showing auto payer as primary

If Auto Insurance is found:

resubmit the claim to Auto insurance

If Auto Insurance is NOT found:

release the claim to the patient (patient responsibility due to missing auto insurance)

2) Check Payer Web Portal (If Access Available)

Some payer portals can show:

• accident-related coverage

• claim-level insurance details

This can help you identify the correct No-Fault payer.

What If Rep Provides No-Fault Carrier Details?

If the payer provides full No-Fault insurance details:

Action Steps:

- Update No-Fault/Auto insurance as Primary

- Resubmit the claim to Primary Auto insurance

- Do not keep Commercial payer as secondary

Key Rule:

Do NOT keep commercial insurance as secondary when No-Fault insurance exists.

Medicare Secondary Billing Rule (MSP Update)

If the patient has Medicare:

Medicare can be kept as secondary.

Once the No-Fault/Auto carrier processes the claim and leaves a balance as patient responsibility:

You can bill Medicare after updating the required MSP information:

Update:

• MSP Code

• Accident indicators (if applicable)

• Proper coordination of benefits

Summary: Best Practice Checklist

Here’s a quick checklist to resolve this denial:

Confirm denial date

Request No-Fault carrier details

If rep has info → collect payer name, policy ID, payer ID, address

Always take claim # and call reference #

If rep doesn’t have info → check system/payment history

Use portal to search auto insurance (if available)

Auto insurance must be PRIMARY

Medicare can be secondary (with MSP code update)

If no auto insurance exists → release claim to patient